LSTM for Multivariate Time Series

Contents

LSTM for Multivariate Time Series#

import numpy as np

import pandas as pd

import torch

from torch import nn

from torch import optim

from typing import Union

import matplotlib.pyplot as plt

Load Data#

We explore the Tesla stock data in our demonstration.

stocks: pd.DataFrame = pd.read_csv("../../data/stocks.csv", index_col=0, parse_dates=True)

company = "TSLA"

stock = stocks.query(f"Company == '{company}'").drop(columns=["Company", "Sector"])

stock

| Open | High | Low | Close | Volume | |

|---|---|---|---|---|---|

| Date | |||||

| 2017-11-02 | 20.008667 | 20.579332 | 19.508667 | 19.950666 | 296871000 |

| 2017-11-03 | 19.966667 | 20.416668 | 19.675333 | 20.406000 | 133410000 |

| 2017-11-06 | 20.466667 | 20.500000 | 19.934000 | 20.185333 | 97290000 |

| 2017-11-07 | 20.068001 | 20.433332 | 20.002001 | 20.403334 | 79414500 |

| 2017-11-08 | 20.366667 | 20.459333 | 20.086666 | 20.292667 | 70879500 |

| ... | ... | ... | ... | ... | ... |

| 2022-10-26 | 219.399994 | 230.600006 | 218.199997 | 224.639999 | 85012500 |

| 2022-10-27 | 229.770004 | 233.809998 | 222.850006 | 225.089996 | 61638800 |

| 2022-10-28 | 225.399994 | 228.860001 | 216.350006 | 228.520004 | 69152400 |

| 2022-10-31 | 226.190002 | 229.850006 | 221.940002 | 227.539993 | 61554300 |

| 2022-11-01 | 234.050003 | 237.399994 | 227.279999 | 227.820007 | 62566500 |

1258 rows × 5 columns

Leave out the last 90 days for testing:

num_days = 90

train_df = stock[:-num_days]

test_df = stock[-num_days:]

Encode Column Names in the Data Frame#

Since the input of PyTorch and Scikit-learn’s model is usually a NumPy array of a tensor, we need to extract the data from Pandas’ data frame by dropping the information of column names and indices, etc.

But we also need the connection between the raw data and its actual meaning. For example, we need to know the original column name of a column vector in the array. Scikit-learn’s LabelEncoder can help us with this.

from sklearn.preprocessing import LabelEncoder

ALL_FEATURES = stock.columns.tolist()

feature_encoder = LabelEncoder()

feature_encoder.fit(ALL_FEATURES)

feature_encoder.classes_

array(['Close', 'High', 'Low', 'Open', 'Volume'], dtype='<U6')

Note

Note that the order of column names in feature_encoder.class_ does not be the same as that in the original data frame!

Now, we transform the data frame to a NumPy array, which is in fact a time series (hence the name train_ts).

# re-order the columns by the column names in the feature encoder

# and then convert it to NumPy array

train_ts = train_df[feature_encoder.classes_].to_numpy()

train_ts

array([[1.99506664e+01, 2.05793324e+01, 1.95086670e+01, 2.00086670e+01,

2.96871000e+08],

[2.04060001e+01, 2.04166679e+01, 1.96753330e+01, 1.99666672e+01,

1.33410000e+08],

[2.01853333e+01, 2.05000000e+01, 1.99340000e+01, 2.04666672e+01,

9.72900000e+07],

...,

[2.36086670e+02, 2.46833328e+02, 2.33826660e+02, 2.34503326e+02,

1.01107500e+08],

[2.35070007e+02, 2.39316666e+02, 2.28636673e+02, 2.37906662e+02,

1.04202600e+08],

[2.45706665e+02, 2.46066666e+02, 2.36086670e+02, 2.37470001e+02,

9.57708000e+07]])

Now, if we want to know what is the meaning of the first column if train_ts, we can use the following code:

# index 0 means the first column

feature_encoder.inverse_transform([0])

array(['Close'], dtype='<U6')

Hence, the first column stores the closing prices.

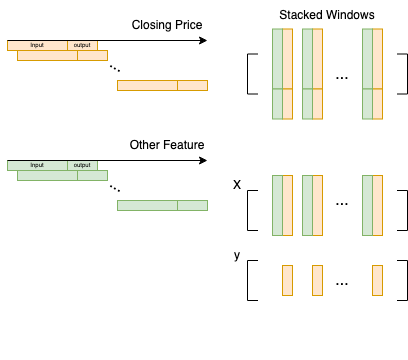

Sliding Windows#

Basically, in our LSTM model, we need to use \(M\) days’ data to predict the closing prices of the next \(N\) days. Hence, we need to slide a window (with size \(M + N\)) across the time series data (imagine a single-variate time series for now), and then stack all the windows together into a large matrix.

The following figure illustrates this idea.

from sklearn.base import BaseEstimator, TransformerMixin

from sklearn.preprocessing import MinMaxScaler

class TimeSeriesTransformer(BaseEstimator, TransformerMixin):

def __init__(

self,

feature_encoder: LabelEncoder,

features: list[str] = ["Close"],

seq_len: int = 10,

pred_len: int = 1,

) -> None:

"""A transformer that transform the time series

to the format suitable for LSTM model.

"""

super().__init__()

self.feature_encoder = feature_encoder

self.features = features

self.seq_len = seq_len

self.pred_len = pred_len

self.scaler = MinMaxScaler(feature_range=(-1, 1))

def fit(

self,

ts: np.ndarray,

split_X_y: bool = True

):

# make sure "Close" is at the end of features

if "Close" in self.features:

self.features.remove("Close")

self.features.append("Close")

# select features of interest

ts = ts[:, self.feature_encoder.transform(self.features)]

# fit min-max scaler to the data

self.scaler.fit(ts)

return self

def transform(

self,

ts: np.ndarray,

split_X_y: bool = True

) -> tuple[np.ndarray, np.ndarray]:

# select features of interest

ts = ts[:, self.feature_encoder.transform(self.features)]

# scale the values of the time series

scaled_ts = self.scaler.transform(ts)

# convert to the format suitable for LSTM

window_size = self.seq_len + self.pred_len if split_X_y else self.seq_len

X_y = np.array([

scaled_ts[i : i + window_size]

for i in range(len(scaled_ts) - window_size + 1)

])

if split_X_y:

X = X_y[:, :-self.pred_len, :]

y = X_y[:, -self.pred_len:, -1]

return X, y

else:

X = X_y

return X

Build LSTM Model#

We use the framework of PyTorch to build an LSTM model for multivariate time series:

class LSTM(nn.Module):

def __init__(

self,

input_size: int,

hidden_size: int,

num_layers: int,

output_size: int

) -> None:

# initialize super class

super().__init__()

self.input_size = input_size

self.hidden_size = hidden_size

self.num_layers = num_layers

self.output_size = output_size

# LSTM layer

self.lstm = nn.LSTM(self.input_size, self.hidden_size, self.num_layers, batch_first=True)

# fully connected layer

self.fc = nn.Linear(self.hidden_size, self.output_size)

def forward(self, x: torch.Tensor) -> torch.Tensor:

"""

Notes:

------

- `output` has shape (N, L, H)

- `h_n` has shape (`num_layers`, N, H)

where

- N is the batch size,

- L is the sequence length, and

- H is the hidden size

"""

output, (h_n, c_n) = self.lstm.forward(x)

# in fact, we want the last hidden value

# from the last LSTM layer, i.e., h_n[-1, :, :]

h = h_n[-1, :, :]

# get predicted value from

# the fully connected layer

y = self.fc.forward(h)

return y

We have also implemented a function to train the LSTM:

def _train(

model: LSTM,

X_train: np.ndarray,

y_train: np.ndarray,

num_epochs: int = 10,

lr: float = 0.01,

quiet=True

) -> float:

# convert to tensors

X_train = torch.Tensor(X_train)

y_train = torch.Tensor(y_train)

# loss function

criterion = nn.MSELoss(reduction="mean")

# optimizer

optimiser = optim.Adam(model.parameters(), lr=lr)

for i in range(num_epochs):

# predicted value

y_pred = model.forward(X_train)

# calculate loss

loss: torch.Tensor = criterion(y_pred, y_train)

if not quiet:

print(f"epoch:\t{i}\tloss:\t{loss}")

# clear gradients

optimiser.zero_grad()

# compute gradients through backward propagation

loss.backward()

# update parameters

optimiser.step()

Note

Note that we put an underscore in the front of this funciton to indicate that it is a private function of this module. We don’t expect users to use this function directly, since in fact we will wrap another class PricePredictor over this LSTM model.

Price Predictor#

Note that there are a lot of hyperparameters to be determined for the LSTM. The idea is that we want to keep the inner central LSTM model as simple as possible. So, we define another class PricePredictor that wraps in the LSTM, and at the same time, provides all possible hyperparameters and other methods like fit and predict that will be exposed to the users.

from sklearn.metrics import r2_score, mean_squared_error

class PricePredictor(BaseEstimator):

feature_encoder: LabelEncoder = None

def __init__(

self,

features: list[str] = ["Close"],

seq_len: int = 10,

pred_len: int = 1,

num_days_ago: int = 100,

hidden_size: int = 32,

num_layers: int = 1,

num_epochs: int = 50,

lr: float = 0.01

) -> None:

"""A model that takes in M days to predict N-day closing prices

where M is `seq_len` and N is `pred_len`.

Parameters

----------

features (list[str], optional): Features of interest. Defaults to ["Close"].

seq_len (int, optional): The number of days needed to predict prices. Defaults to 10.

pred_len (int, optional): The number of days of closing prices to predict. Defaults to 1.

num_days_ago (int, optional): The latest few days of the provided trainig date to consider. Defaults to 100.

hidden_size (int, optional): Hidden size of LSTM. Defaults to 32.

num_layers (int, optional): Number of layers of LSTM. Defaults to 1.

num_epochs (int, optional): Number of epochs to train. Defaults to 10.

lr (float, optional): Learning rate. Defaults to 0.01.

Raises

------

Exception: Missing feature encoder.

"""

super().__init__()

# initialize feature encoder

if PricePredictor.feature_encoder is None:

raise Exception("Feature encoder must be proveded as a class attribute.")

self.features = features

self.seq_len = seq_len

self.pred_len = pred_len

self.num_days_ago = num_days_ago

self.hidden_size = hidden_size

self.num_layers = num_layers

self.num_epochs = num_epochs

self.lr = lr

# underlying LSTM model

self.model: LSTM = None

# time series transformer

self.ts_transformer: TimeSeriesTransformer = None

# the last sequence of input time series with length `self.seq_len`

self.last_seq: np.ndarray = None

# metric / method of scoring

self.metric: str = "R2"

# R2 score

self.rs: float = None

# mean squared error

self.mse: float = None

def _get_input_size(self) -> int:

"""Find the input size for the LSTM model.

Returns

-------

int: Input size.

"""

input_size = len(self.features)

if "Close" not in self.features:

input_size += 1

return input_size

def fit(self, ts: np.ndarray, quiet=True):

"""Fit the model.

Parameters

----------

ts (np.ndarray): Training time series.

quiet (bool, optional): If `quiet` is `False` then training losses will be printed in the terminal.

Defaults to True.

"""

# initialize LSTM model

self.model = LSTM(

input_size=self._get_input_size(),

hidden_size=self.hidden_size,

num_layers=self.num_layers,

output_size=self.pred_len

)

# initialize time series transformer

self.ts_transformer = TimeSeriesTransformer(

feature_encoder=self.feature_encoder,

features=self.features,

seq_len=self.seq_len,

pred_len=self.pred_len

)

# only keep the last few days

ts = ts[-self.num_days_ago:]

# store the last sequence of the time series for prediction

self.last_seq = ts[-self.seq_len:].copy()

# get X and y

X, y = self.ts_transformer.fit_transform(ts)

# train LSTM model

_train(

model=self.model,

X_train=X,

y_train=y,

num_epochs=self.num_epochs,

lr=self.lr,

quiet=quiet

)

def score(self, test_ts: np.ndarray) -> float:

"""Compute the fitting score.

Parameters

----------

test_ts (np.ndarray): Test time seires.

Returns

-------

float:

1. R2 score is returned by default.

2. If the computation of R2 score fails, then the negative MSE is returned.

"""

# get true prices

test_ts = test_ts[:self.pred_len]

test_ts = test_ts[:, self.feature_encoder.transform(["Close"])]

y_true = test_ts.flatten()

# predicted prices

y_pred = self.predict()

# mean squred error

self.mse = mean_squared_error(y_true, y_pred)

if len(y_pred) >= 2:

self.r2 = r2_score(y_true, y_pred)

return self.r2

else:

self.metric = "Negative MSE"

return -self.mse

def predict(

self,

ts: Union[np.ndarray, None] = None

) -> np.ndarray:

"""Predict the prices of future N days if no input is provided

where n equals the attribute `pred_len`.

If a time series (M days) is passed to this function,

then each time the function will take one of M days

to predict the prices of the next N days.

So, there will be (M + 1) batches of N-day prices.

Parameters

----------

ts (Union[np.ndarray, None], optional): A time series consisting of future data.

Defaults to None.

Returns

-------

np.ndarray:

1. If the input is `None`, then a 1-D NumPy array of future N-day prices is returned.

2. If there is an input time series, then an (M + 1)-by-N NumPy array is returned.

"""

# a flag indicating whether there is an input time series

is_empty_input = ts is None

if is_empty_input:

ts = self.last_seq

else:

# attach the input time series

# to the last sequence of data

ts = np.concatenate((self.last_seq, ts))

# transform the time series

X = self.ts_transformer.transform(ts, split_X_y=False)

# convert to tensor

X = torch.Tensor(X).detach()

# predit with LSTM model

y_pred: torch.Tensor = self.model.forward(X)

# convert to NumPy array

y_pred = y_pred.detach().numpy()

# rescale the predicted values to prices

sliding_prices: np.ndarray = np.apply_along_axis(

self._to_price,

axis=1,

arr=y_pred

)

if is_empty_input:

# return a 1-D array of future N-day prices

price = sliding_prices[0]

return price

else:

# return (M + 1) baches of N-day prices

return sliding_prices

def _to_price(self, y_pred: np.ndarray) -> np.ndarray:

"""Recover the price from the scaled data.

Parameters

----------

y_pred (np.ndarray): Predicted values ranging from -1 to 1.

Returns

-------

np.ndarray: Prices.

"""

price_min = self.ts_transformer.scaler.data_min_[-1]

price_range = self.ts_transformer.scaler.data_range_[-1]

feature_min, feature_max = self.ts_transformer.scaler.feature_range

price = price_min + (y_pred - feature_min) * price_range / (feature_max - feature_min)

return price

Fine-Tune the Model: Randomized Search#

The common methods of tuning the hyperparameters are grid search and randomized search. For grid search, we will need to fit a model for every combination of possible parameters, which is extremely time-consuming. In practice, it is pref red to use randomized search.

In out project, we intend use Scikit-learn’s RandomizedSearchCV to do the randomized search. As described in the official documentation, our estimator / model needs to implement fit and score methods, which we have already done this in the previous section.

We define a function train that implements the randomized search to train our model:

from sklearn.model_selection import TimeSeriesSplit, RandomizedSearchCV

def train(

stocks: pd.DataFrame,

company: str,

num_days_left_out: int = 90,

pred_len: int = 1

) -> dict:

feature_encoder = LabelEncoder()

feature_encoder.fit(ALL_FEATURES)

df = stocks.query(f"Company == '{company}'")

train_df = df[:-num_days_left_out]

train_df = train_df[ALL_FEATURES]

train_ts = train_df[feature_encoder.classes_].to_numpy()

# a sliding window splitter for time series cross validation

ts_cv = TimeSeriesSplit(

n_splits=2,

test_size=pred_len

)

# initialize a price predictor model

PricePredictor.feature_encoder = feature_encoder

price_predictor = PricePredictor(pred_len=pred_len)

# use random search to tune the model

search = RandomizedSearchCV(

price_predictor,

{

"features": [

["Close"],

["Close", "Open"],

["Close", "Open", "Volume"]

],

"seq_len": [

30, 60, 90

],

"num_days_ago": [

300, 400, 500

],

"hidden_size": [

16, 32

],

"num_layers": [

1, 2

]

},

cv=ts_cv,

n_iter=10,

verbose=2

)

# train!

search.fit(train_ts)

# return the training result

train_result = {

"model": search.best_estimator_,

"params": search.best_params_,

"score": search.best_score_

}

return train_result

Finally, we are ready to train the model:

Note

The following cell is not executable since we discover that something may go wrong when one execute this notebook online. Therefore, we display execution output from our machine in the following.

stocks: pd.DataFrame = pd.read_csv("../../data/stocks.csv", index_col=0, parse_dates=True)

company = "TSLA"

stock = stocks.query(f"Company == '{company}'").drop(columns=["Company", "Sector"])

train_result = train(stocks, company="TSLA", num_days_left_out=num_days, pred_len=1)

train_result

The output is as follows:

Fitting 2 folds for each of 10 candidates, totalling 20 fits

[CV] END features=['Close', 'Open'], hidden_size=32, num_days_ago=300, num_layers=2, seq_len=60; total time= 5.4s

[CV] END features=['Close', 'Open'], hidden_size=32, num_days_ago=300, num_layers=2, seq_len=60; total time= 4.6s

[CV] END features=['Close'], hidden_size=16, num_days_ago=300, num_layers=2, seq_len=30; total time= 1.6s

[CV] END features=['Close'], hidden_size=16, num_days_ago=300, num_layers=2, seq_len=30; total time= 1.6s

[CV] END features=['Close', 'Open', 'Volume'], hidden_size=32, num_days_ago=500, num_layers=1, seq_len=60; total time= 3.8s

[CV] END features=['Close', 'Open', 'Volume'], hidden_size=32, num_days_ago=500, num_layers=1, seq_len=60; total time= 4.0s

[CV] END features=['Close'], hidden_size=32, num_days_ago=500, num_layers=2, seq_len=90; total time= 10.6s

[CV] END features=['Close'], hidden_size=32, num_days_ago=500, num_layers=2, seq_len=90; total time= 9.9s

[CV] END features=['Close', 'Open'], hidden_size=32, num_days_ago=400, num_layers=2, seq_len=90; total time= 8.9s

[CV] END features=['Close', 'Open'], hidden_size=32, num_days_ago=400, num_layers=2, seq_len=90; total time= 9.1s

[CV] END features=['Close'], hidden_size=32, num_days_ago=500, num_layers=1, seq_len=30; total time= 1.9s

[CV] END features=['Close'], hidden_size=32, num_days_ago=500, num_layers=1, seq_len=30; total time= 1.8s

[CV] END features=['Close'], hidden_size=32, num_days_ago=400, num_layers=1, seq_len=90; total time= 4.1s

[CV] END features=['Close'], hidden_size=32, num_days_ago=400, num_layers=1, seq_len=90; total time= 4.1s

[CV] END features=['Close'], hidden_size=16, num_days_ago=400, num_layers=1, seq_len=60; total time= 1.7s

[CV] END features=['Close'], hidden_size=16, num_days_ago=400, num_layers=1, seq_len=60; total time= 1.7s

[CV] END features=['Close', 'Open', 'Volume'], hidden_size=16, num_days_ago=400, num_layers=1, seq_len=60; total time= 1.9s

[CV] END features=['Close', 'Open', 'Volume'], hidden_size=16, num_days_ago=400, num_layers=1, seq_len=60; total time= 1.9s

[CV] END features=['Close'], hidden_size=32, num_days_ago=400, num_layers=1, seq_len=30; total time= 1.7s

[CV] END features=['Close'], hidden_size=32, num_days_ago=400, num_layers=1, seq_len=30; total time= 1.6s

{'model': PricePredictor(features=['Open', 'Volume', 'Close'], num_days_ago=500,

pred_len=3, seq_len=60),

'params': {'seq_len': 60,

'num_layers': 1,

'num_days_ago': 500,

'hidden_size': 32,

'features': ['Close', 'Open', 'Volume']},

'score': -3.7899972418662307}

# load trained model

price_predictor: PricePredictor = train_result["model"]

Alternatively, we have implemented a function load_price_predictor in our lstm.py moduel to load a pre-trained model.

import sys

sys.path.append("../../")

# import our modules

import lstm

# load pre-trained model

price_predictor: PricePredictor = lstm.load_price_predictor("../../models/TSLA-3-day-predictor.pkl")

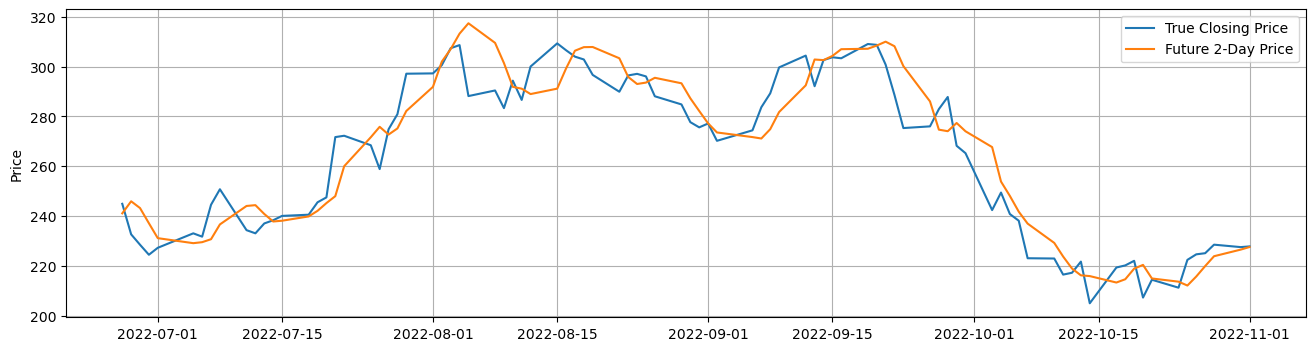

# transform the test data

test_ts = test_df[feature_encoder.classes_].to_numpy()

t = test_df.index

y_true = test_df["Close"].to_numpy()

sliding_prices = price_predictor.predict(test_ts)

# possible values for num_days_ahead are 1, 2 and 3

num_days_ahead = 2

# since the model predict the future prices up to 3 days,

# here we only need the future 2-day price

y_pred = sliding_prices[:-1, num_days_ahead - 1]

# plot the result

plt.figure(figsize=(16, 4))

plt.plot(t, y_true, label="True Closing Price")

plt.plot(t, y_pred, label=f"Future {num_days_ahead}-Day Price")

plt.ylabel("Price")

plt.legend()

plt.grid()

plt.show()